I Bought a Condo In Thailand For Less Than $100,000 (10 Things I Checked Before Signing)

From 93k in debt to my first property abroad

Six years ago, I moved abroad with 93,000 euros in debt.

I won’t repeat the whole story here (you can read about it here).

But it took me four years to work my way out of it.

And about two years ago, I was sitting in my usual coffee shop in Chiang Mai after a morning ride in the mountains.

There were other cyclists there who just come back from riding too.

I said hello to one of them.

His name is Paul.

He owns a real estate agency in Chiang Mai for over 20 years.

We started riding together.

Over a few weeks, he walked me through how the Thai property market actually works:

What yields look like

How the rental market moves

What separates a “good building” from a bad one.

At some point I asked him to show me some condos.

He told me what to check, what to skip, and what most buyers get wrong.

I probably learned more from Paul in a few rides than most people learn before they make the decision to buy property overseas.

Since I actually had some cash sitting around, I thought maybe I should put it to work.

I ended up buying a condo a few weeks later, for less than $100,000.

But before I signed anything, I had a checklist.

(Lists are a big part of my life, if I had to make a list of things that make me calmer, “lists” would be on top of that list.)

I verified a lot of things before purchasing, and today I’m sharing those with you.

Why I Bought (And Why Chiang Mai)

At the time, I invested “like everyone else”.

My portfolio mostly consisted of ETFs, stocks, and crypto.

But I never owned property.

After talking to Paul for a few weeks, I liked the idea of putting money into something I could actually “walk through” and that’s not just sitting as a digital number on a screen.

And after looking at all the facts about the Thai rental market, I got curious.

Rental yields on condos in Chiang Mai sit between 4% and 8%, depending on the building, how well you furnish it and whether you are renting out short term or long term.

Also, I was living in Thailand anyhow and was on my way to my long-term golden visa when I started looking.

Buying in the country where I actually live made sense.

I can visit the building myself, meet the seller, go to the land office in person.

The condo I ended up buying was maybe 15 minutes from my apartment.

I could check on the renovation, deal with problems in person, and keep an eye on things without booking a flight.

At that point, there was no “grand strategy” yet.

I simply had cash, local knowledge, and the math worked.

If you’re an American 50+ with a meaningful retirement nest egg and you’re seriously thinking about retiring abroad in the next 0–5 years, hit reply and write “RETIRE”.

You’ll get a private invite to the “Retire Abroad Priority List” with some of my best tactics for retiring abroad.

What Most People Get Wrong

The first thing Paul told me when I said I was interested in buying was:

“Ben, the numbers need to work out.”

If you walk into a condo, love the view and the vibe, that’s great.

But if the numbers don’t add up, the view doesn’t mean much.

A nice unit with a view might return 4% while a less pretty one in a better location returns 7%.

Buy for yield, not for how it looks in photos.

Emotional buying is probably the most common mistake you can make purchasing property abroad (at least when you’re buying as an investment).

Paul flagged some other things too.

Buying doesn’t always means “owning”.

There are terms like freehold, leasehold, usufruct, foreign ownership quotas.

In some countries your “ownership” expires after 30 years.

In others, foreigners can buy condos but not land.

You need to know what you’re actually purchasing before you wire money.

I was lucky because Paul was already a friend by the time I bought.

He told me the truth because he wasn’t trying to close a deal (most buyers don’t have that).

Another thing to keep in mind is total cost.

Apart from the purchase price of the property / the condo, there are other factors you need to consider.

Transfer fees, taxes, legal costs, currency conversion, furnishing, renovation (just to name a few).

All of that eats into your first-year yield if you only budget for the purchase price.

I wrote about currency risk specifically, because it caught me off guard too.

Also, you need to think about your exit strategy.

What happens when you want to sell?

Is the resale market liquid?

What are the exit costs?

Can your heirs inherit the property, or does local law complicate that?

Some might bring up Thailand-specific risks, like earthquakes, the Cambodia situation, political instability.

I’ve been through two earthquakes in Thailand, one in Bangkok and one in Chiang Mai.

This is what insurance is for.

As for geopolitical tension, there are conflicts all over the world right now.

If you’re waiting for a country with zero risk, you can buy in New Zealand or Iceland (good luck with budgeting in those).

Every country has trade-offs.

What matters is that you know what you’re getting into before you sign.

So I made a list.

10 things I checked before I put any money down.

As always, written from lived experience.

The 10 Things I Checked Before Signing

Here’s what was on my list.

1. Ownership type

In Thailand, foreigners can’t own land.

But you can own a condo in your own name, freehold, as long as the building is registered as a condominium.

Some are classified as “apartments”, which looks the same but don’t give you freehold ownership as a foreigner.

There’s also a cap, meaning foreign ownership in any building can’t exceed 49% of the total floor area.

I asked the juristic office (the body that manages the building) for a written letter confirming there was still space in the quota before I put any money down.

This applies way beyond Thailand.

Every country has its own version of this.

Different ownership structures, different restrictions on what foreigners can buy, different rules on how long your ownership lasts.

In some places what you’re “buying” is really a 30-year lease.

Make sure you understand what you’re actually getting before you commit to anything.

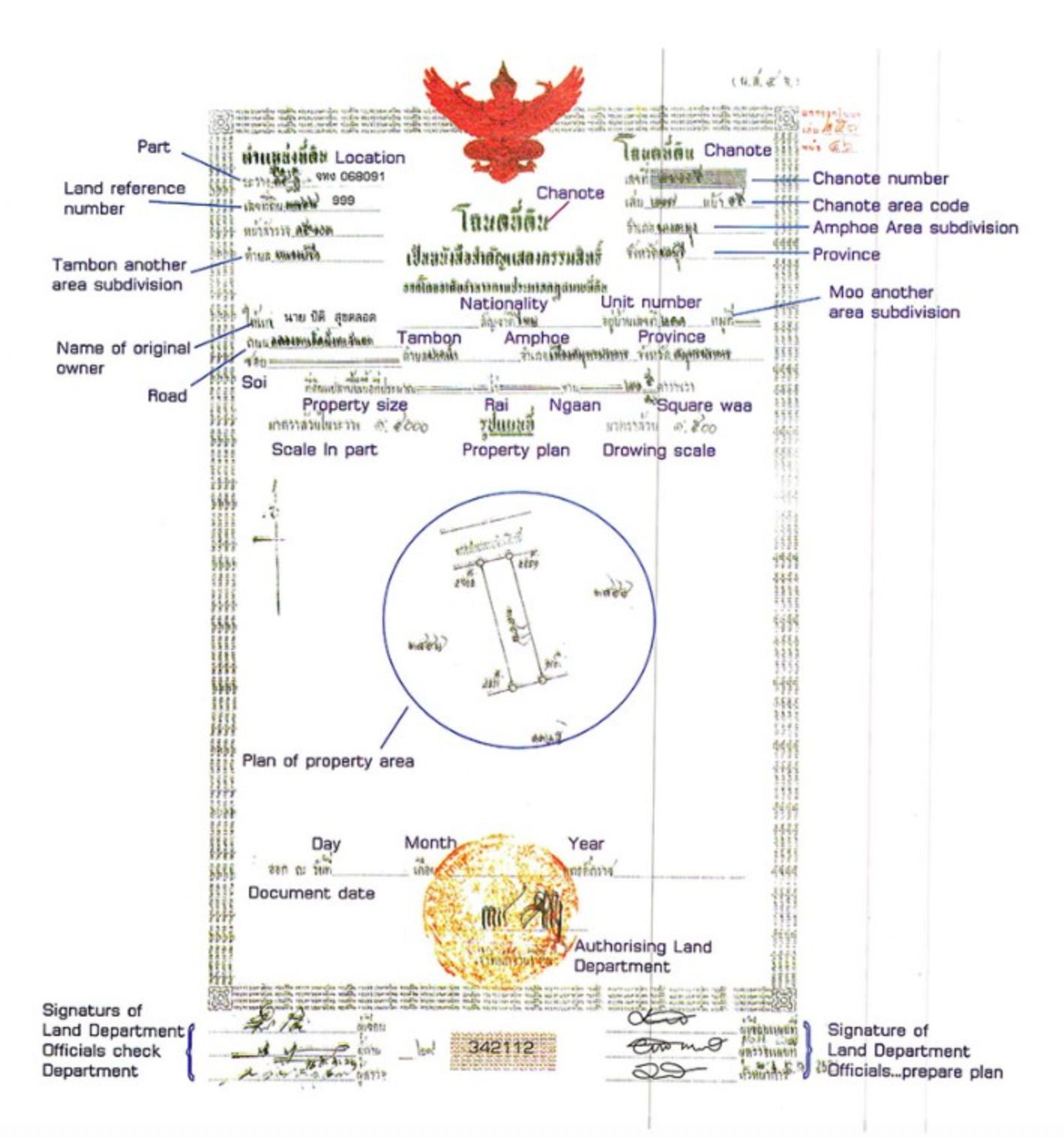

2. Title deed and seller

Paul told me to check the “title deed type”.

In Thailand, the one you need is called a Chanote.

It’s the highest level of land title, gives you full rights, and has properly surveyed boundaries.

There are “lesser titles” that are weaker legally and less precise on where your property actually starts and ends.

Whatever country you’re buying in, the title system will look different.

In Portugal there’s a land registry called Conservatória.

In Mexico, you’re dealing with a notario público and the public registry.

The names change, the process changes, but the question is always the same:

Does the person selling this actually own it, and is it clean of obligations?

3. How your money gets there

Thailand requires you to wire the purchase funds from overseas in a foreign currency.

The bank in Thailand converts it to baht and issues something called a Foreign Exchange Transaction form, or FET.

You bring that form to the land office when you transfer the title. If you don’t have that form, you won’t get the title deed transferred in your name.

I had to coordinate with my bank, get through KYC checks, and raise my transfer limits.

It took some back and forth over a few weeks, but it got done.

Most countries have specific rules about how foreign money enters for a property purchase: