93 Dutch Politicians Just Voted to Steal From Their Citizens' Portfolios

The new 36% tax on unrealized gains, what it means for expats, and the countries where your investments are still safe

On February 12, 2026, the Dutch House of Representatives voted to tax money that doesn’t yet exist.

The bill is called the “Actual Return in Box 3 Act” and replaces a system that taxed investments based on “assumed” returns, a framework the Dutch Supreme Court ruled unconstitutional in a series of decisions beginning in December 2021.

93 politicians voted yes (75 votes were needed).

Starting January 1, 2028:

Dutch residents will owe 36% on the annual increase in value of their stocks, bonds, and crypto.

The bill still needs Senate approval.

But the parties that voted yes in the House hold a majority in the Senate too.

This is (most likely) happening.

The Kobeissi Letter’s tweet about it pulled over 15 million views (as of time of writing this):

Shopify’s CEO called it “the dumbest thing any government on planet earth is pursuing right now.”

But most of the coverage stopped at outrage.

Nobody explained what this actually means if you are an investor, an expat, or someone planning a move abroad.

As usual, the internet did what the internet does:

Plenty of outrage and zero solutions.

Which is why the focus of today’s article will be:

What happened in the Netherlands, how the tax works, and why it breaks every rule in the book

The broader pattern and why such laws usually end up affecting the “average person”

The countries where your investment gains are still taxed at zero or at least not at crazy rates that make investment unsustainable

Let’s start.

Stuck on your moving abroad process? You can book an hour with me here.

How The Dutch Tax System Works

The Netherlands taxes income in three separate buckets, called “boxes.”

Box 1 covers employment income and homeownership.

Box 2 covers income from owning a significant share (5%+) in a company.

Box 3 covers savings and investments.

Box 3 is where this gets ugly.

Until now, the Dutch government didn’t tax your actual investment returns.

Instead, they assumed you earned a “fixed percentage” on your assets and taxed that fictional number (which is absurd already).

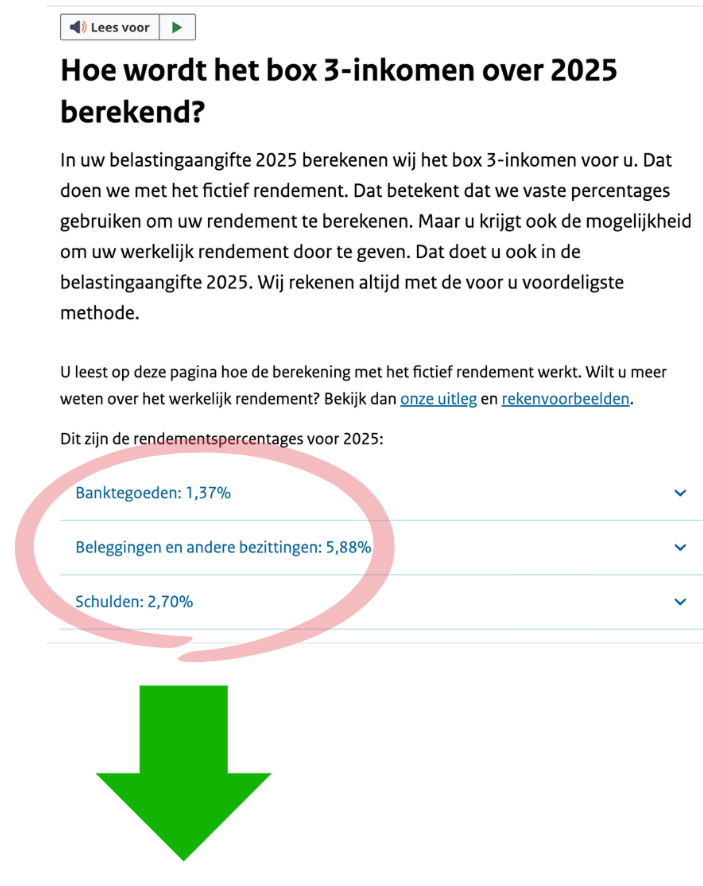

In 2025, the government assumed you earned 5.88% on your investments.

Translation:

“How is Box 3 income for 2025 calculated?

These are the return percentages for 2025:

Bank deposits: 1.37% Investments and other assets: 5.88% Debts: 2.70%”

The Problem With This Calculation

If you portfolio dropped 15% you still owe tax on gains that never existed.

Which is why in December 2021, the Dutch Supreme Court said that’s illegal.

Taxing people on money they did not earn does not make any sense.

The ruling forced the government to refund billions in overpaid taxes and come up with a new system.

Their solution was to tax actual returns instead.

Which sounds reasonable.

But what they came up with, is completely backwards.

The new law taxes all actual returns at a flat 36%.

That includes dividends, interest, and rent you actually received.

But it also includes the annual increase in value of stocks, bonds, and crypto you didn’t sell.

If your portfolio goes up €50,000 on paper, you owe €17,352 to the government.

Without selling a single share.

There are some concessions:

€1,800 tax-free threshold on annual returns

Losses above €500 can be carried forward indefinitely

Real estate and startup shares (companies under 5 years old with less than €30 million in revenue) are exempt from the unrealized gains portion.

But let's be honest.

Those are cosmetics to disguise the fact that the government is plugging a €2.3 billion budget hole with their citizens' portfolios.

And here the kicker:

State Secretary for Taxation Eugène Heijnen admitted during parliamentary debate that the government would have preferred to tax only realized gains.

But he said this won’t be feasible by 2028.

Taxing unrealized gains was easier to implement and fix the annual budget hole.

Let that sink in.

The government chose this system not because of fairness, but because it was faster.

If you’re an American 50+ with a meaningful retirement nest egg and you’re seriously thinking about retiring abroad in the next 0–5 years, hit reply and write “RETIRE”.

You’ll get a private invite to the “Retire Abroad Priority List” with some of my best tactics for retiring abroad.

A Brief History of Taxing Your Gains

Capital gains tax has been around for over a century.

The US started taxing investment profits in 1913.

The UK introduced it in 1965.

Most developed countries followed over the next few decades.

The logic was always simple.

You buy something.

You sell it for more than you paid.

You owe taxes on the difference.

The key word is sell.

Taxes are only due when money actually enters your account.

Some countries skip this tax entirely.

Singapore has no capital gains tax.

Neither does New Zealand, Hong Kong or the UAE.

Belgium doesn’t tax individual stock market gains.

Switzerland doesn’t tax capital gains for private investors.

And then there are the countries that pushed too hard and paid for it.

When Governments Got Greedy

France ran a wealth tax from 1982 to 2017.

It was called the ISF (Solidarity Tax on Wealth).

Between 2000 and 2017, this led to around 60,000 millionaires leaving the country.

Total capital flight between 1988 and 2007 was estimated at €200 billion.

GDP growth dropped by an estimated 0.2% every year because of it.

French economist Eric Pichet calculated that the exodus cost the government nearly twice the revenue the wealth tax actually generated.

Governments took notice:

Macron killed it in 2018.

Germany scrapped its wealth tax in 1997.

Denmark the same year.

Sweden in 2007.

Finland in 2006.

Austria in 1994.

Every single one faced the same problem:

Aggressive taxation pushed capital + people out faster than revenue came in.

And just to be clear:

This is not an argument against taxing wealth.

Wealthy people should pay their fair share.

But when the tax is designed so badly that the wealthy leave (because they have more freedom of mobility), guess what happens next?

Everyone else (who stays) picks up the bill.

By now you might think:

Ben, where does the Netherlands fit in all of this?

My main point is this.

Every country I just mentioned, whether they tax gains at 0% or 40%, shares one thing in common:

They tax you when you sell.

The Netherlands just abandoned that principle.

They want to tax before you sell.

No major economy has pulled this off.

And the reason is always the same:

A number on a screen is not money in the bank.

The Netherlands is going to learn this lesson the hard way.

Where Your Investments Are Still Safe

Not every country treats people like an ATM.

Here are some places where capital gains are taxed at zero or close to it:

UAE (0%) No income tax, no capital gains tax, no inheritance tax.

Singapore (0%) No capital gains tax on stocks, bonds, or crypto. However, getting in is not easy.

New Zealand (0%) No formal capital gains tax on shares or most assets. Income tax tops out at 39%, but portfolio growth is untaxed.

Hong Kong (0%) No capital gains tax, no dividend tax, income tax capped at 15%.

Panama (0% on foreign gains) Territorial tax system. Anything earned outside Panama is untaxed. Plenty of attractive visa options to chose from.

One thing to remember:

Americans are taxed on worldwide income no matter where they live.

Moving abroad won’t change that.

But foreign residency should at least not make your life more complicated.

Conclusion

That’s it.

I hope this gave you some clarity on what's actually happening and what your options are.

Three things worth remembering:

The Netherlands is about to tax wealth that only exists on a screen. This is NOT a tax just on the wealthy, but something that will affect the average citizen.

Countries that tried aggressive wealth taxation watched their richest residents leave and leave the rest of the population with the bill.

There are still countries where your investments grow at reasonable rates. Getting residency in one of them is easier than most people think.

That’s it for this week.

Thanks for reading, and as always, appreciate having you here.

— Ben

PS

If you are an American 50+ and want to emigrate within the next 0-5 years, and don’t want to navigate healthcare, banking, visas, taxes and country selection by yourself, reply to this mail with “RETIRE”.

You’ll get an invite to the “Retire Abroad Priority List” with some of my best tactics for retiring abroad.

This is a very helpful synopsis of some of the tax laws. I've already decided that I want to look at investing outside of the USA when I when I take the leap next year. I don't trust the current government to not collapse the market. And I would think it would make sense to spread my money around a little bit to help offset changes in the value of the dollar.... So I will be reaching out to you when the time comes.

Most laws like this are created for the Proles to get behind and applaud. 'Tax The Rich' is always popular and ensure it gets passed without too much fuss, but its usually a foot in the door. Then over the years a small inconsequential amendment here and there and next thing you know it only applies to the Proles and the rich have a nice work-around that only clever and expensive accountants and tax consultants can navigate....... C'est la vie